Fill in Your Vermont S 3 Form

Fill in Your Vermont S 3 Form

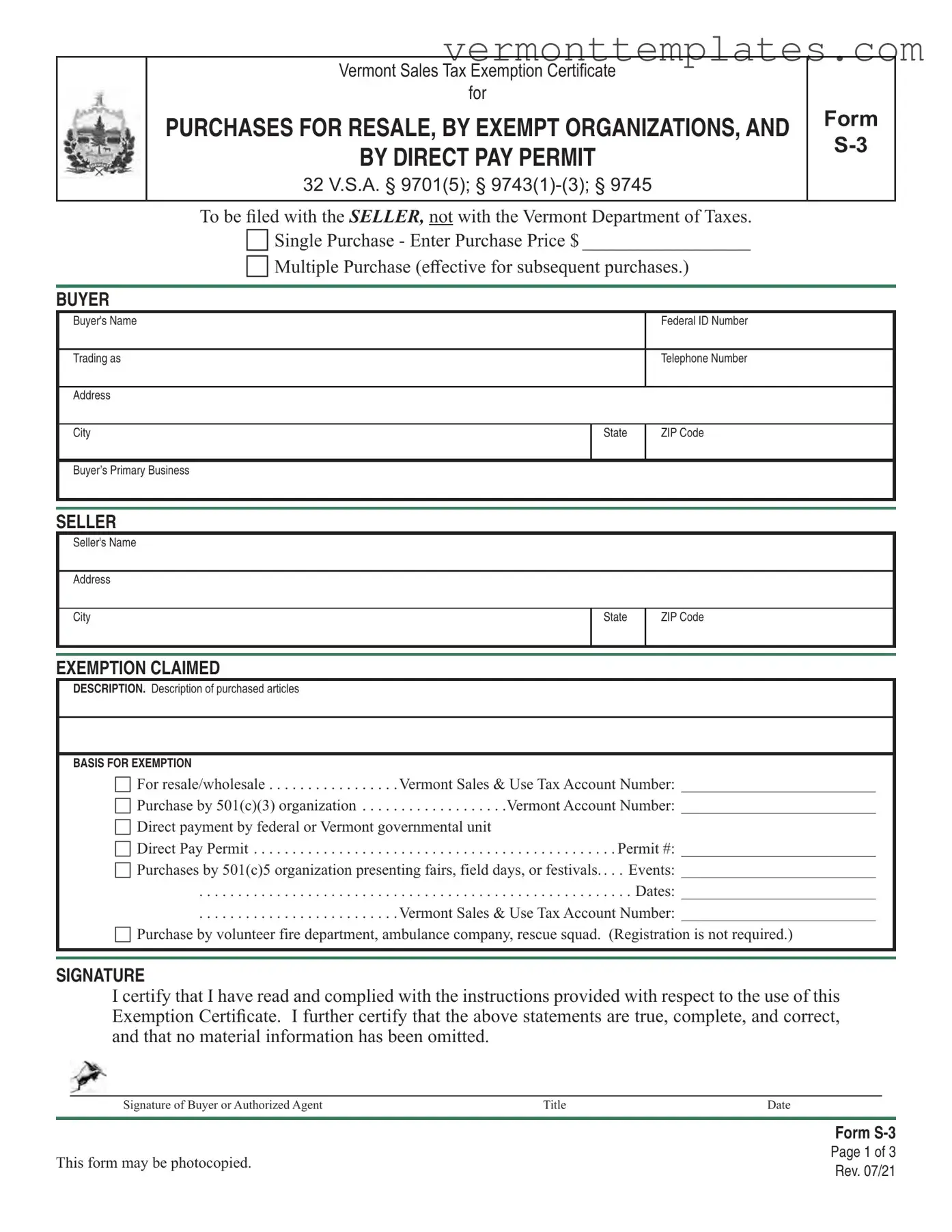

The Vermont S-3 form serves as a crucial tool for buyers seeking sales tax exemptions on specific purchases. This form is primarily designed for individuals and organizations making purchases for resale or those classified as exempt entities, such as 501(c)(3) organizations. Buyers must present this form to the seller, not to the Vermont Department of Taxes. The S-3 form accommodates both single and multiple purchases, allowing for flexibility depending on the buyer's needs. Key sections include the buyer's information, the seller's details, and a description of the purchased items. Buyers must also indicate the basis for their exemption, which can range from resale purposes to purchases made by government units or volunteer emergency services. It is essential that the form is completed accurately, as it includes a certification statement affirming the truthfulness of the provided information. Sellers accepting the S-3 form in good faith are protected from liability regarding sales tax collection, provided they adhere to specific conditions outlined in the form's instructions. Understanding the proper use of the Vermont S-3 form can significantly benefit both buyers and sellers by ensuring compliance with state tax regulations while facilitating tax-exempt transactions.

When filling out the Vermont S-3 form, there are important dos and don'ts to keep in mind. Adhering to these guidelines can ensure a smooth process and help avoid potential issues.

The Vermont Sales Tax Exemption Certificate (Form S-3) is similar to the New York State Resale Certificate. Both documents allow businesses to purchase goods without paying sales tax, provided those goods are intended for resale. In New York, the resale certificate must be presented to the seller at the time of purchase, just as the S-3 form requires in Vermont. Both forms also necessitate that the buyer provides their tax identification number, ensuring that the seller can verify the buyer’s eligibility for the exemption.

Another comparable document is the California Resale Certificate. This certificate serves a similar purpose, allowing retailers to buy products tax-free if they plan to resell them. Like the S-3 form, the California version requires the buyer to fill out their business information and provide a seller’s permit number. Both documents protect sellers from liability for collecting sales tax on exempt transactions, provided they accept the certificates in good faith.

The Texas Sales and Use Tax Resale Certificate also shares similarities with the Vermont S-3 form. In Texas, businesses can use this certificate to purchase items intended for resale without incurring sales tax. The Texas form requires the buyer’s name, address, and sales tax permit number, mirroring the information required on the S-3 form. Both documents also emphasize that the buyer must use the purchased items for the intended purpose to qualify for the exemption.

The Florida Annual Resale Certificate is another document that aligns with the Vermont S-3 form. This certificate allows businesses to make multiple tax-exempt purchases throughout the year. Similar to the S-3 form, the Florida certificate requires the buyer to provide their business details and tax identification number. Both forms aim to streamline the purchasing process for businesses that frequently buy items for resale, reducing the administrative burden of obtaining a new certificate for each transaction.

Understanding various sales tax exemption certificates is crucial for businesses looking to maximize savings while complying with tax regulations. For instance, the Vermont Sales Tax Exemption Certificate (Form S-3) mirrors the New York State Resale Certificate, allowing businesses to purchase goods tax-free when intended for resale. Similarly, the California Resale Certificate and the Texas Sales and Use Tax Resale Certificate serve the same purpose, each requiring specific business information to confirm eligibility. The Florida Annual Resale Certificate enables multiple tax-exempt purchases throughout the year, while the Illinois and Massachusetts certificates also provide businesses with opportunities to avoid sales tax on goods intended for resale. This understanding is essential not only for compliance but also for ensuring a smooth business operation. For more information about related documents, visit https://arizonapdf.com/transfer-on-death-deed.

The Illinois Resale Certificate is also comparable to the Vermont S-3 form. In Illinois, businesses can use this certificate to buy items without paying sales tax if they are intended for resale. Like the S-3, the Illinois certificate requires the buyer to provide their business name and identification number. Both documents serve to protect sellers from the obligation to collect sales tax when valid resale certificates are presented at the time of sale.

Lastly, the Massachusetts Sales Tax Resale Certificate functions similarly to the Vermont S-3 form. This certificate allows businesses to purchase goods for resale without incurring sales tax. The Massachusetts form requires the buyer to provide their business information and sales tax registration number, akin to the requirements of the S-3 form. Both documents help ensure that sales tax is only collected on final consumer sales, thus supporting businesses in their resale operations.

Failing to Provide Complete Information: Buyers often leave sections blank, especially the purchase price or the Vermont Sales & Use Tax Account Number. Incomplete forms can lead to delays or rejections.

Using an Incorrect Form: Some individuals mistakenly use forms other than the Vermont S-3 for exemption claims. Ensure that the correct form is being utilized to avoid complications.

Not Signing the Form: A signature is required from the buyer or an authorized agent. Neglecting to sign the form invalidates the exemption claim.

Misunderstanding Eligibility: Buyers sometimes claim exemptions for purchases that do not qualify. For instance, contractors cannot use this form for materials used in construction.

Incorrectly Claiming Multiple Purchases: When using the multiple purchase option, buyers often fail to ensure that each purchase links back to the exemption certificate. Proper documentation is essential.

Failing to Present the Certificate Timely: The exemption certificate must be presented at or before the time of purchase. Delayed submission can result in the loss of the exemption.

Ignoring Retention Requirements: Sellers must retain exemption certificates for at least three years. Buyers sometimes forget this, which can lead to issues if the seller is audited.

Vermont Sales Tax Exemption Certificate

for

PURCHASES FOR RESALE, BY EXEMPT ORGANIZATIONS, AND

BY DIRECT PAY PERMIT

32 V.S.A. § 9701(5); §

FORM

To be filed with the SELLER, not with the Vermont Department of Taxes.

Single Purchase - Enter Purchase Price $ __________________

Multiple Purchase (effective for subsequent purchases.)

BUYER

Buyer's Name |

|

Federal ID Number |

|

|

|

Trading as |

|

Telephone Number |

|

|

|

Address |

|

|

|

|

|

City |

State |

ZIP Code |

|

|

|

Buyer’s Primary Business |

|

|

|

|

|

|

|

|

SELLER

Seller's Name

Address

City |

State |

ZIP Code |

|

|

|

|

|

|

EXEMPTION CLAIMED

DESCRIPTION. Description of purchased articles

BASIS FOR EXEMPTION |

|

|

For resale/wholesale |

Vermont Sales & Use Tax Account Number: _________________________ |

|

Purchase by 501(c)(3) organization |

. . . . . . . . . . . . . .Vermont Account Number: _________________________ |

|

Direct payment by federal or Vermont governmental unit |

|

|

Direct Pay Permit |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

Permit #: _________________________ |

Purchases by 501(c)5 organization presenting fairs, field days, or festivals. . . |

. Events: _________________________ |

|

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . Dates: _________________________ |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

Vermont Sales & Use Tax Account Number: _________________________ |

|

Purchase by volunteer fire department, ambulance company, rescue squad. (Registration is not required.)

SIGNATURE

I certify that I have read and complied with the instructions provided with respect to the use of this Exemption Certificate. I further certify that the above statements are true, complete, and correct, and that no material information has been omitted.

Signature of Buyer or Authorized Agent |

Title |

Date |

Form

This form may be photocopied. |

Page 1 of 3 |

|

Rev. 07/21 |

||

|

FORM

Vermont Sales Tax Exemption Certificate for

Purchases for Resale, by Exempt Organizations, and by Direct Pay Permit

This exemption certificate does not apply to contractors.

General Information

Please print in BLUE or BLACK ink only.

This exemption certificate applies to the following:

•Purchase(s) of tangible personal property for the purpose of resale

•Purchase(s) by an organization which is designated as a 501(c)(3) by the Internal Revenue Service, or agricultural organizations qualified for exempt status under § 501(c)(5) when presenting agricultural fairs, field days, or festivals

•Purchase(s) by a Federal or Vermont governmental unit (direct payment)

•Purchase(s) using a Direct Pay Permit

•Purchase(s) by a volunteer fire department, ambulance company, or rescue squad

Please note: Civic, social, recreational, and business league organizations are not 501(c)(3) organizations, and therefore cannot make exempt purchases.

Accepting an Exemption Certificate in “Good Faith”

The buyer must present to the seller an accurate and properly executed exemption certificate for the exempted sale. The responsibility is on the seller to determine if the buyer is submitting the exemption certificate in “good faith.” This requires the seller to be familiar with Vermont Sales and Use Tax law and regulations, including exemptions, that apply to the seller’s business. If the buyer provides a certificate that is not valid, i.e., the item purchased does not qualify for the exemption, this is not in good faith and the seller should not accept the certificate. When the seller accepts the certificate in good faith, the seller is not liable for collecting and remitting Vermont Sales Tax.

An exemption certificate is received at the time of sale in good faith when all of the following conditions are met:

•The certificate contains no statement or entry which the seller knows, or has reason to know, is false or misleading.

•The certification is on an exemption form issued by the Vermont Department of Taxes or a form with substantially identical language.

•The certificate is signed, dated and complete (all applicable sections and fields completed).

•The property purchased is of a type ordinarily used for the stated purpose, or the exempt use is explained.

Form

Page 2 of 3 Rev. 07/21

Burden of Proof

The burden of proof is on the seller to demonstrate the certificate was taken in good faith. If the seller cannot provide an exemption certificate showing that the sale was exempt, the Department will seek to collect tax from the seller. If, however, the seller can prove the buyer’s claim for the exemption was false, the Department will seek to collect the tax from the buyer.

Obtaining the Exemption Certificate

The seller must obtain an exemption certificate from the buyer either prior to or at the time of the sale. If the certificate is not available at the time of sale, the seller has 90 days after the sale to obtain a fully executed certificate, accepted in good faith.

Retaining the Exemption Certificate

Sellers must retain exemption certificates for at least three years from the date of the last sale covered by the certificate to document why the tax was not collected from the buyer.

Multiple Purchase Exemption Certificates

If the buyer presents a “Multiple Purchase” exemption certificate to the seller, it may be used only when purchasing tangible personal property for use as indicated on this exemption certificate. For each purchase covered by the exemption certificate, the sales slip or invoice must show the buyer’s name and address sufficient to link the purchase to the exemption certificate on file.

Other types of exemption certificates that may be applicable are available on our website at

For questions regarding how these exemption certificates may be properly applied, please contact the Vermont Department of Taxes at (802)

Form

Page 3 of 3 Rev. 07/21

The Vermont S-3 form is a vital document for buyers seeking sales tax exemptions for certain purchases. However, it is often accompanied by other forms and documents that further clarify or support the exemption claims. Below is a list of these additional documents, each serving a specific purpose in the exemption process.

Understanding these additional forms and documents can streamline the exemption process and ensure compliance with Vermont tax regulations. By being well-prepared, buyers can navigate their purchasing needs effectively while taking full advantage of their exemption rights.

Vt Sales Tax - The form captures vital contractor and seller information, ensuring compliance.

Vermont Ethics Network - Consult resources like “Taking Steps” for additional support in planning.

Understanding the implications of a Release of Liability waiver is crucial for protecting your interests in any activity that involves inherent risks. This form delineates the responsibilities which participants emphasize, ensuring all parties acknowledge the potential hazards involved.

Addendum Meaning in Real Estate - The seller guarantees that the property will be free from liens and encumbrances.