Fill in Your Vermont Bi 472 Form

Fill in Your Vermont Bi 472 Form

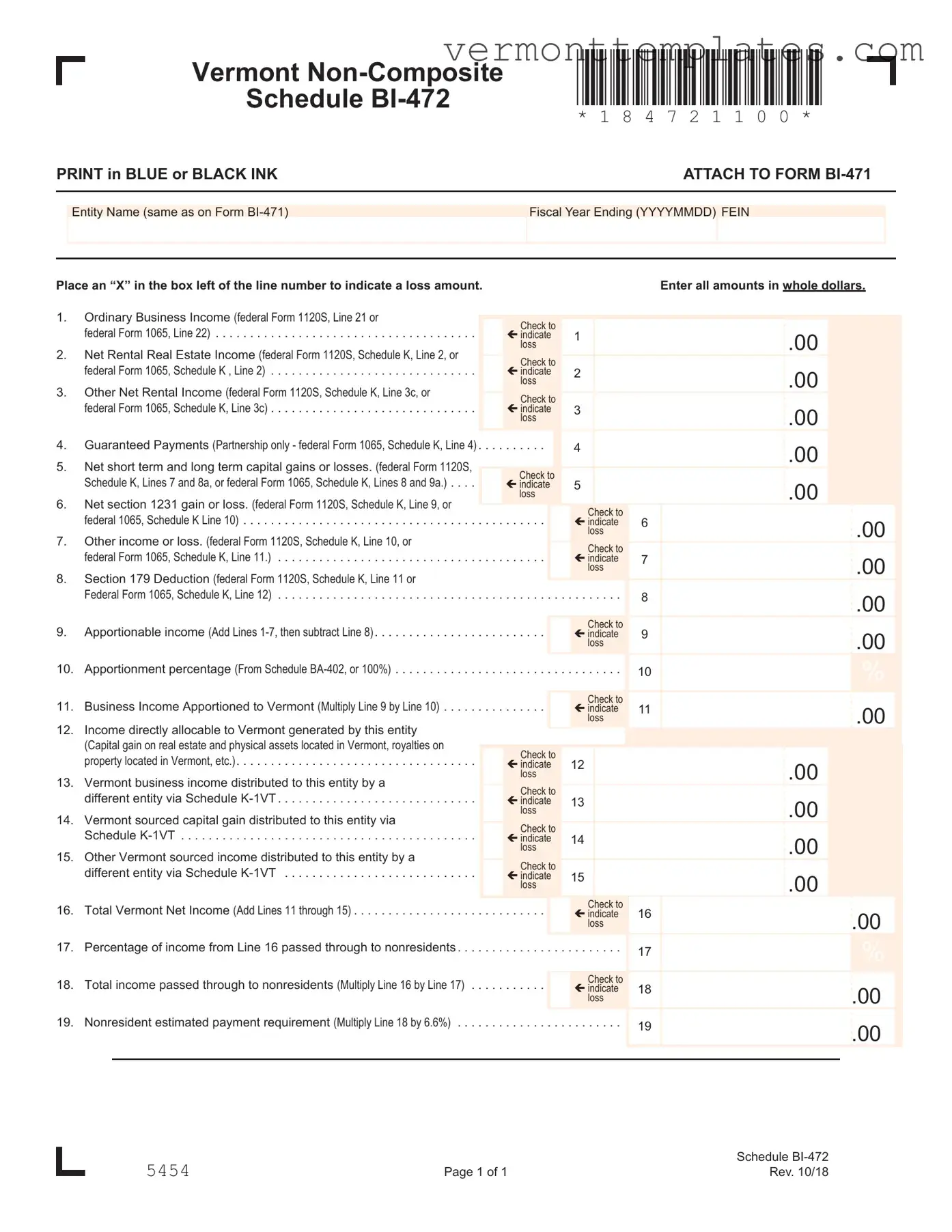

The Vermont BI-472 form is a crucial document for entities operating within the state, particularly for those that are filing as partnerships or S corporations. This form captures essential financial information, including ordinary business income, net rental income, and capital gains or losses. It requires the entity to provide various income figures, such as guaranteed payments and section 179 deductions, which directly affect the overall tax liability. Additionally, the form facilitates the apportionment of income to Vermont, allowing businesses to determine their tax obligations accurately. By detailing income sources and ensuring that all amounts are reported in whole dollars, the BI-472 helps maintain transparency and compliance with state tax regulations. Entities must also account for any income passed through to nonresidents, which adds another layer of complexity to the filing process. Completing this form accurately is essential for ensuring that businesses meet their tax responsibilities while maximizing potential deductions.

When filling out the Vermont BI-472 form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are nine things you should and shouldn't do:

The Vermont BI-472 form is similar to the federal Form 1120S, which is used by S corporations to report income, deductions, and credits. Both forms require businesses to provide a detailed account of their ordinary business income and other income sources. The structure of these forms is similar, as they both break down income into specific categories, such as rental income and capital gains. This allows for a clear comparison of financial performance and ensures that the income reported aligns with federal requirements.

Another document that resembles the Vermont BI-472 is the federal Form 1065. This form is designed for partnerships and also captures various types of income and deductions. Like the BI-472, it includes sections for reporting guaranteed payments and net rental income. Both forms help ensure that the income is accurately apportioned to the appropriate state, making it easier for entities to comply with state tax laws while also aligning with federal regulations.

The Schedule K-1 is also akin to the Vermont BI-472 form. This document provides detailed information about each partner's share of income, deductions, and credits from a partnership. Similar to the BI-472, the K-1 breaks down income sources, allowing for clarity in reporting. Both documents serve the purpose of distributing income to individual partners or shareholders, ensuring that everyone involved understands their tax obligations based on the entity's overall performance.

The Vermont Schedule BA-402 is another document that shares similarities with the BI-472. This form is used to calculate apportionment percentages for businesses operating in multiple states. Both forms require careful calculations to determine how much income is attributable to Vermont. By using these forms together, businesses can ensure that they are accurately reporting their income and complying with state tax laws.

Form 4797, which is used to report the sale of business property, is also comparable to the Vermont BI-472. Both forms address capital gains and losses, allowing businesses to report their financial outcomes from property sales. The inclusion of capital gains in both forms highlights the importance of tracking these transactions for tax purposes, ensuring that businesses can accurately report their financial activities.

The federal Schedule E is similar as well, as it is used to report supplemental income and loss. This form captures income from rental real estate, partnerships, and S corporations, much like the BI-472. Both forms require detailed reporting of various income sources, making it easier for taxpayers to compile their financial information in one place for tax reporting.

In the realm of financial documentation, clarity and standardization are paramount, and various forms serve to streamline this process, such as the smarttemplates.net, which provides templates that can aid in organizing essential applicant information, thereby refining the job application process across different sectors.

Lastly, the Vermont Form BI-471 is closely related to the BI-472. While the BI-471 serves as the main business income tax return, the BI-472 provides additional details about specific income types. Both forms work together to ensure comprehensive reporting of a business's financial activities, helping to maintain transparency and compliance with state tax regulations.

Not using blue or black ink. It's important to follow the instruction to ensure clarity.

Failing to attach the form to Form BI-471. This step is necessary for proper processing.

Entering amounts in cents instead of whole dollars. All figures should be rounded to whole dollars.

Overlooking the requirement to place an “X” in the box next to the line number for loss amounts. This indicates whether a loss is being claimed.

Not including the entity name as it appears on Form BI-471. Consistency is key for identification.

Incorrectly calculating the apportionable income. Make sure to add Lines 1-7 and subtract Line 8 accurately.

Missing the apportionment percentage from Schedule BA-402. This percentage is essential for determining Vermont income.

Neglecting to check the boxes for lines indicating losses. This can lead to misunderstandings in the processing of the form.

Forgetting to calculate the nonresident estimated payment requirement correctly. This is calculated by multiplying Line 18 by 6.6%.

|

|

|

|

|

Vermont |

|

|

|

*184721100* |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

Schedule |

|

|

|

* 1 8 4 7 2 1 1 0 0 * |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

PRINT in BLUE or BLACK INK |

|

|

|

|

|

|

|

ATTACH TO FORM |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Entity Name (same as on Form |

|

Fiscal Year Ending (YYYYMMDD) |

FEIN |

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Place an “X” in the box left of the line number to indicate a loss amount. |

|

|

|

|

|

|

|

Enter all amounts in whole dollars. |

|

||||||||||||||

1. |

|

Ordinary Business Income (federal Form 1120S, Line 21 or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

federal Form 1065, Line 22) |

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

||||||||

2. |

|

Net Rental Real Estate Income (federal Form 1120S, Schedule K, Line 2, or |

|

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

Check to |

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

federal Form 1065, Schedule K , Line 2) |

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||

3. |

|

Other Net Rental Income (federal Form 1120S, Schedule K, Line 3c, or |

|

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

Check to |

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

federal Form 1065, Schedule K, Line 3c) |

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|

|

|

|

|

|||||

4. |

|

Guaranteed Payments (Partnership only - federal Form 1065, Schedule K, Line 4) |

4 |

|

|

.00 |

|

|

|

|

|

|

|

||||||||||

5. |

|

Net short term and long term capital gains or losses. (federal Form 1120S, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

Schedule K, Lines 7 and 8a, or federal Form 1065, Schedule K, Lines 8 and 9a.). . . |

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

||||||||

6. |

|

Net section 1231 gain or loss. (federal Form 1120S, Schedule K, Line 9, or |

|

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

Check to |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

federal 1065, Schedule K Line 10) |

|

6 |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

||||||||||||||

7. |

|

Other income or loss. (federal Form 1120S, Schedule K, Line 10, or |

|

|

|

loss |

|

|

|

|

|

|

|||||||||||

|

|

|

|

Check to |

7 |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

federal Form 1065, Schedule K, Line 11.) |

|

ç indicate |

|

|

.00 |

|

|

|||||||||||||

8. |

|

Section 179 Deduction (federal Form 1120S, Schedule K, Line 11 or |

|

|

|

loss |

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

Federal Form 1065, Schedule K, Line 12) |

8 |

|

|

.00 |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

9. |

|

Apportionable income (Add Lines |

|

Check to |

9 |

|

|

|

|

|

|

|

|

|

|||||||||

|

|

ç indicate |

|

|

.00 |

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|||||||

10. |

Apportionment percentage (From Schedule |

10 |

|

|

|

|

% |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

11. |

Business Income Apportioned to Vermont (Multiply Line 9 by Line 10) |

|

Check to |

11 |

|

|

|

|

|

|

|

|

|

||||||||||

|

ç indicate |

|

|

.00 |

|

|

|||||||||||||||||

12. |

Income directly allocable to Vermont generated by this entity |

|

|

|

loss |

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

(Capital gain on real estate and physical assets located in Vermont, royalties on |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

property located in Vermont, etc.) |

|

Check to |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

13. |

Vermont business income distributed to this entity by a |

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

different entity via Schedule |

|

13 |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

14. |

Vermont sourced capital gain distributed to this entity via |

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

Schedule |

|

14 |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

15. |

Other Vermont sourced income distributed to this entity by a |

|

loss |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Check to |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

different entity via Schedule |

|

15 |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

ç indicate |

|

|

.00 |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

loss |

Check to |

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

16. |

Total Vermont Net Income (Add Lines 11 through 15) |

|

16 |

|

|

|

|

|

|

|

|

|

|||||||||||

|

ç indicate |

|

|

.00 |

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|

||||||

17. |

Percentage of income from Line 16 passed through to nonresidents |

|

17 |

|

|

|

|

% |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

18. |

Total income passed through to nonresidents (Multiply Line 16 by Line 17) |

|

Check to |

|

|

|

|

|

|

|

|

|

|

||||||||||

|

ç indicate |

18 |

|

|

.00 |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

loss |

|

|

|

|

|

|

||||||

19. |

Nonresident estimated payment requirement (Multiply Line 18 by 6.6%) |

|

19 |

|

|

.00 |

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5454 |

|

Schedule |

Page 1 of 1 |

Rev. 10/18 |

The Vermont BI-472 form is used to report business income for entities operating in Vermont. When filing this form, there are several other documents that may also be required to provide additional information or support. Below are some common forms that often accompany the BI-472.

Each of these forms plays a crucial role in ensuring that the business income is reported correctly and that the tax obligations are met. It is important to complete all required forms accurately to avoid potential issues with tax compliance.

Vermont Tax - This registration can potentially grant access to various state resources and support for new businesses.

Vt Dcf - The insurance company may respond to the DMV regarding policy coverage details.

When engaging in the sale of an all-terrain vehicle in California, it is crucial to utilize the California ATV Bill of Sale form to ensure that all necessary details are documented properly. This form not only facilitates a smooth transaction but also provides essential proof of ownership transfer, which can be vital for registration and any legal considerations. For those looking for comprehensive documentation, you can find resources for various transactions including the ATV Bill of Sale in All California Forms.

Addendum Meaning in Real Estate - Understanding this addendum is key for a successful property transaction.