Fill in Your S 3M Vermont Form

Fill in Your S 3M Vermont Form

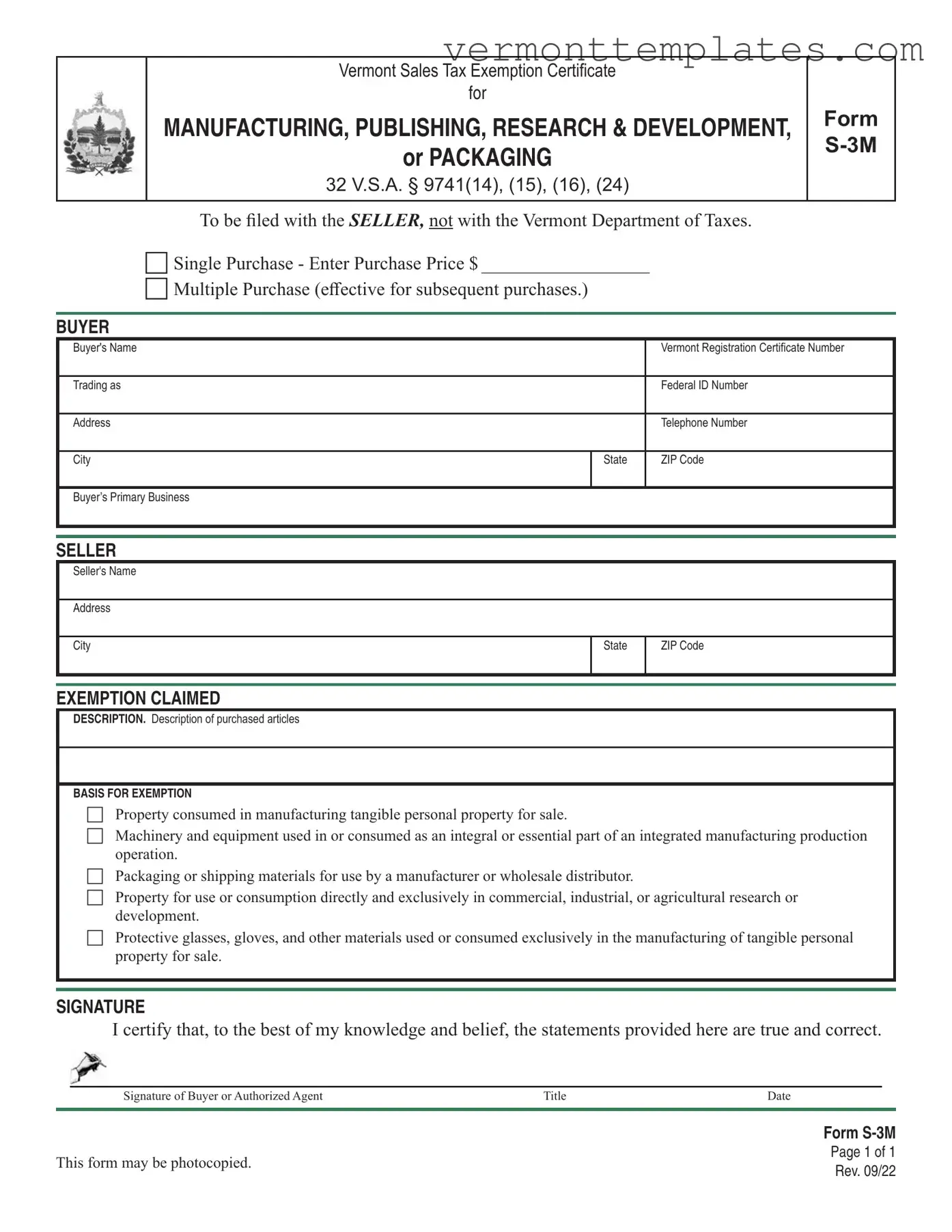

The S 3M Vermont form is an important tool for businesses involved in manufacturing, publishing, research and development, or packaging. This form serves as a Sales Tax Exemption Certificate, allowing eligible buyers to claim exemptions on certain purchases. It is essential for sellers to have this certificate on file, as it helps them avoid tax liabilities on transactions that qualify for exemption under Vermont law. The form requires the buyer's name, address, and business registration details, ensuring that only qualified entities can benefit from the exemption. Buyers can indicate whether the exemption is for a single purchase or multiple purchases, which can simplify future transactions. The S 3M form also outlines specific categories of property that qualify for exemption, including machinery and equipment used directly in the manufacturing process, as well as packaging materials. Buyers must certify that the information provided is accurate and true, adding a layer of responsibility to the process. It’s important to note that the seller must retain these certificates for a minimum of three years, ensuring compliance with state regulations. Overall, understanding the S 3M form is crucial for businesses to effectively manage their tax obligations while taking advantage of available exemptions.

When filling out the S-3M Vermont form, it is essential to follow certain guidelines to ensure accuracy and compliance. Here are five things you should and shouldn't do:

The S-3M Vermont form shares similarities with the IRS Form 4506-T, which is used to request a transcript of tax returns. Both documents require the identification of the requester and the purpose of the request. While the S-3M focuses on tax exemption for specific purchases in manufacturing and related fields, Form 4506-T is aimed at obtaining tax information for various purposes, such as loan applications or audits. Each form emphasizes the importance of accurate information and requires a signature to validate the request.

Another comparable document is the IRS Form W-9, which is used to provide taxpayer identification information. Similar to the S-3M, the W-9 requires the name, address, and taxpayer identification number of the individual or business. Both forms serve as essential tools for ensuring compliance with tax regulations. While the S-3M is specifically for claiming exemptions in Vermont, the W-9 is often used in various transactions to confirm the status of the taxpayer.

The Sales Tax Exemption Certificate, commonly used in many states, is also akin to the S-3M form. This certificate allows buyers to purchase goods without paying sales tax if the items are intended for resale or specific uses. Like the S-3M, the Sales Tax Exemption Certificate requires details about the buyer and the nature of the exemption being claimed. Both documents are essential in maintaining proper tax compliance and ensuring that sellers are protected from tax liabilities.

For those managing real estate and seeking a simplified process of transferring property, it's important to consider options such as the Transfer-on-Death Deed, which can be filled out by visiting https://arizonapdf.com/transfer-on-death-deed, ensuring that beneficiaries receive the intended assets without the complications of probate court or traditional wills.

Form ST-5, used in Massachusetts, is another document similar to the S-3M. This form serves as a sales tax exemption certificate for purchases made by exempt organizations. Both forms require the buyer's information and the specific exemption being claimed. They both aim to facilitate tax-exempt purchases while providing a legal safeguard for sellers against tax collection responsibilities.

In New York, the ST-121 Exempt Use Certificate is comparable to the S-3M. This form allows businesses to claim exemption from sales tax on purchases made for resale or specific exempt purposes. The structure of both forms is similar, requiring the buyer's details and the nature of the exemption. Both are crucial in ensuring that tax laws are followed while allowing businesses to operate without the burden of unnecessary tax costs.

The Certificate of Exemption for Nonprofit Organizations, often used in various states, parallels the S-3M in that it allows qualifying organizations to make tax-exempt purchases. Both documents necessitate the identification of the organization and the reason for the exemption. They serve as vital tools for nonprofits, ensuring that they can allocate resources effectively without incurring additional tax expenses.

The Resale Certificate is another document that resembles the S-3M. This certificate allows businesses to purchase goods intended for resale without paying sales tax. Both forms require the buyer's information and a declaration of the intended use of the purchased items. They are critical for maintaining compliance with tax laws while enabling businesses to operate efficiently.

Lastly, the IRS Form 8832, which is used to elect how an entity is classified for federal tax purposes, shares some common ground with the S-3M. Both forms require specific information about the entity involved and must be signed to be valid. While the S-3M is focused on state-level sales tax exemptions, Form 8832 addresses federal tax classifications, highlighting the importance of accurate documentation in tax-related matters.

Incomplete Information: Failing to provide all required details, such as the buyer's name, address, and registration numbers, can lead to delays or rejection of the exemption claim.

Incorrect Exemption Claimed: Selecting the wrong exemption category can result in the denial of the certificate. It’s essential to ensure that the claimed exemption matches the actual use of the purchased items.

Missing Signature: Not signing the form or having an unauthorized person sign can invalidate the certificate. Always ensure that the signature is from the buyer or an authorized agent.

Failure to Date the Form: Not including the date on which the form is completed can lead to complications. The date is crucial for establishing the validity of the exemption.

Using the Wrong Form: Submitting the S-3M form instead of the appropriate form for specific purchases, like fuel or electricity, can result in tax liabilities. Verify that the correct form is being used for the intended purchase.

Not Retaining the Certificate: Sellers must keep the exemption certificate for at least three years. Failing to retain this document can lead to issues if the transaction is questioned later.

Vermont Sales Tax Exemption Certificate

for

MANUFACTURING, PUBLISHING, RESEARCH & DEVELOPMENT, FORM |

|

or PACKAGING |

|

|

|

32 V.S.A. § 9741(14), (15), (16), (24) |

|

To be filed with the SELLER, not with the Vermont Department of Taxes.

Single Purchase - Enter Purchase Price $ __________________

Multiple Purchase (effective for subsequent purchases.)

BUYER

Buyer's Name |

|

Vermont Registration Certificate Number |

|

|

|

Trading as |

|

Federal ID Number |

|

|

|

Address |

|

Telephone Number |

|

|

|

City |

State |

ZIP Code |

|

|

|

Buyer’s Primary Business |

|

|

|

|

|

|

|

|

SELLER

Seller's Name

Address

City |

State |

ZIP Code |

|

|

|

|

|

|

EXEMPTION CLAIMED

DESCRIPTION. Description of purchased articles

BASIS FOR EXEMPTION

Property consumed in manufacturing tangible personal property for sale.

Machinery and equipment used in or consumed as an integral or essential part of an integrated manufacturing production operation.

Packaging or shipping materials for use by a manufacturer or wholesale distributor.

Property for use or consumption directly and exclusively in commercial, industrial, or agricultural research or development.

Protective glasses, gloves, and other materials used or consumed exclusively in the manufacturing of tangible personal property for sale.

SIGNATURE

I certify that, to the best of my knowledge and belief, the statements provided here are true and correct.

Signature of Buyer or Authorized Agent |

Title |

Date |

Form

This form may be photocopied. |

Page 1 of 1 |

|

Rev. 09/22 |

||

|

FORM

Vermont Sales Tax Exemption Certificate for

Manufacturing, Publishing, Research & Development, or Packaging

General Information

Please print in BLUE or BLACK ink only.

Tangible personal property is property which can be seen, touched, and measured.

The term “distributor” does not include retailers selling directly to the ultimate consumer. Retail stores of all kinds and restaurants are not included in the terms “manufacturer” or “distributor.”

Tangible personal property that becomes an ingredient or component part of, or is consumed or destroyed in the manufacture of property for sale is exempt. Further, machinery and equipment used in or

consumed as an integral or essential part of an integrated production operation by a manufacturing plant is exempt. Where manufacturing begins and ends is described in 32 V.S.A. § 9741(14). Pre- manufacturing and

Form

Accepting an Exemption Certificate in “Good Faith”

The buyer must present to the seller an accurate and properly executed exemption certificate for the exempted sale. The responsibility is on the seller to determine if the buyer is submitting the exemption certificate in “good faith.” This requires the seller to be familiar with Vermont Sales and Use Tax law and regulations, including exemptions, that apply to the seller’s business. If the buyer provides a certificate that is not valid, i.e., the item purchased does not qualify for the exemption, this is not in good faith and the seller should not accept the certificate. When the seller accepts the certificate in good faith, the seller is not liable for collecting and remitting Vermont Sales Tax.

An exemption certificate is received at the time of sale in good faith when all of the following

conditions are met:

•The certificate contains no statement or entry which the seller knows, or has reason to know, is false or misleading.

•The certification is on an exemption form issued by the Vermont Department of Taxes or a form with substantially identical language.

•The certificate is signed, dated and complete (all applicable sections and fields completed).

•The property purchased is of a type ordinarily used for the stated purpose, or the exempt use is explained.

Form

Page 1 of 2 Rev. 09/22

Improper Certificate / Lack of Certificate

Sales transactions which are not supported by properly executed exemption certificates shall be deemed to be taxable retail sales. The burden of proof that the tax was not required to be

collected is upon the SELLER.

Retention of Certificates

Certificates must be retained by the seller for a period of not less than three (3) years from the date of the last sale covered by the certificate.

Additional Purchases by Same Buyer

If the buyer presents a “Multiple Purchase” exemption certificate to the seller, it may be used only when purchasing tangible personal property for use as indicated on this exemption certificate. For each purchase covered by the exemption certificate, the sales slip or invoice must show the buyer’s name and address sufficient to link the purchase to the exemption certificate on file.

Form

Page 2 of 2 Rev. 09/22

The S 3M Vermont form is a crucial document for businesses engaged in manufacturing, publishing, research and development, or packaging. It serves as a sales tax exemption certificate that allows eligible buyers to make tax-exempt purchases. However, several other forms and documents often accompany the S 3M to ensure compliance and clarity in transactions. Below is a brief overview of these related documents.

Understanding these additional forms is vital for businesses seeking to navigate Vermont's tax regulations effectively. Each document plays a specific role in ensuring compliance and facilitating tax exemptions. Proper use of these forms can save businesses time and money while maintaining adherence to state laws.

Taxable Supplies - Tax professionals often use this form to assist businesses in complying with Vermont's tax regulations.

Vermont State Board of Nursing - If you don’t have a Social Security Number, submit your passport number instead.

To navigate the complexities of becoming an authorized lottery retailer in Florida, it is crucial to understand the requirements outlined in the Florida Lottery DOL-129 form. This comprehensive document not only covers the application process and associated fees but also highlights the need for a thorough background investigation and the necessity of posting a bond or other security. For those seeking more information and resources related to Florida forms, visit All Florida Forms, which can provide additional guidance and assistance in fulfilling these important obligations.

Vt Sales Tax - Filing the S-3C properly helps in avoiding unnecessary tax collection disputes.