Fill in Your S 3C Vermont Form

Fill in Your S 3C Vermont Form

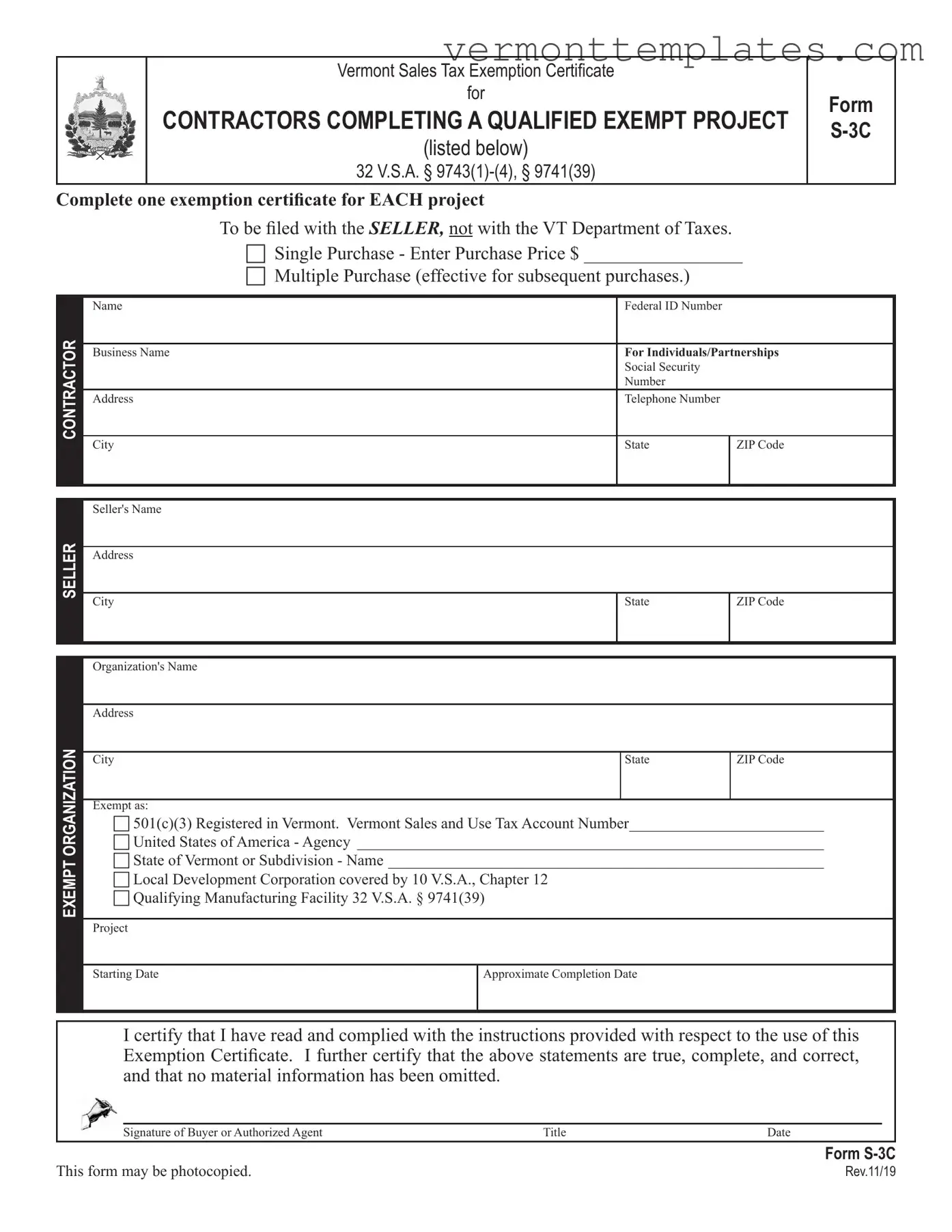

The S 3C Vermont form serves as a vital tool for contractors engaged in projects that qualify for sales tax exemptions. This form is specifically designed for contractors who are completing work for exempt organizations, such as government entities or 501(c)(3) nonprofits. By filling out this certificate, contractors can avoid paying sales tax on materials and supplies that will be incorporated into the project, provided that these items are used in a manner that aligns with the regulations set forth by the Vermont Department of Taxes. Each project requires its own exemption certificate, which must be submitted to the seller at the time of purchase, rather than to the state tax department. The form gathers essential information, including the contractor's business details, the seller's information, and the specifics of the project, such as its start and completion dates. It also outlines the types of organizations and projects that qualify for exemptions, emphasizing that not all nonprofit projects will be eligible. Understanding the nuances of this form can help contractors navigate the complexities of Vermont's tax laws and ensure compliance while taking advantage of available tax benefits.

When filling out the S 3C Vermont form, it’s essential to be meticulous. Here’s a list of things you should and shouldn’t do to ensure a smooth process:

By following these guidelines, you can help ensure that your exemption process goes as smoothly as possible. Pay attention to the details, and don’t hesitate to reach out for clarification if needed.

The IRS Form 501(c)(3) application is similar to the S 3C Vermont form in that both are used to establish and confirm the tax-exempt status of organizations. The IRS Form 501(c)(3) is specifically for nonprofit organizations seeking federal tax exemption. Like the S 3C form, it requires detailed information about the organization, including its purpose and activities. Both forms aim to ensure that the entity qualifies for tax benefits based on their charitable, educational, or public service missions.

The Sales Tax Exemption Certificate (STEC) is another document that parallels the S 3C form. The STEC allows buyers to purchase goods without paying sales tax if they meet certain criteria. Similar to the S 3C, it requires the buyer to provide information about the exempt purpose of their purchase. Both forms serve to document the tax-exempt status of purchases and ensure compliance with tax regulations.

The Contractor Exemption Certificate (CEC) is also akin to the S 3C form, as it is specifically designed for contractors working on projects for exempt organizations. The CEC allows contractors to purchase materials without incurring sales tax, provided the materials are used in qualifying projects. Like the S 3C form, the CEC requires the contractor to certify the nature of the project and the exempt status of the organization involved.

The Form ST-5, used in Massachusetts, is comparable to the S 3C Vermont form. This form allows for sales tax exemption on certain purchases made by exempt organizations. Both forms require similar information, including the purchaser's details and the specific exempt purpose for the transaction. The intent behind both forms is to streamline the process for exempt organizations to acquire necessary goods without the burden of sales tax.

The New York State Exempt Organization Certificate (Form ST-119.1) shares similarities with the S 3C form as well. This certificate allows exempt organizations to purchase goods and services without paying sales tax. Both forms require the organization to provide proof of their exempt status and details regarding the nature of the purchases. The primary goal is to facilitate tax-free transactions for qualifying entities.

The Illinois Sales Tax Exemption Certificate is another document that functions similarly to the S 3C form. This certificate allows eligible organizations to make tax-exempt purchases. Like the S 3C, it requires the organization to declare its exempt status and the purpose of the purchase. Both forms help ensure that the tax-exempt entities can operate without the financial burden of sales tax on necessary purchases.

When preparing to apply for various tax exemptions, organizations may find it beneficial to utilize an Employment Application PDF form, as it can help in providing structured and standardized information essential for establishing eligibility. Such documents, including those available at smarttemplates.net, play a crucial role in outlining the necessary details about an organization's operations, ensuring that all required information is consolidated effectively to facilitate the application process.

The Form ST-2 in New Jersey is comparable to the S 3C form as well. This form allows for the exemption of sales tax for certain organizations and purchases. Both forms require the buyer to assert their tax-exempt status and detail the nature of the goods or services being purchased. They serve to ensure compliance with state tax laws while facilitating necessary transactions for exempt organizations.

Finally, the Pennsylvania Exempt Use Certificate is similar to the S 3C form in its purpose of allowing tax-exempt purchases. This certificate requires the buyer to provide information about their exempt status and the intended use of the purchased items. Both forms are designed to simplify the purchasing process for organizations that qualify for tax exemptions, ensuring compliance with state tax regulations.

Failing to complete a separate form for each project: Each project requires its own exemption certificate. Submitting one form for multiple projects can lead to confusion and potential denial of the exemption.

Not providing the correct seller information: Ensure that the seller's name and address are accurately filled out. Incorrect details can complicate the verification process.

Neglecting to include the Vermont Sales and Use Tax account number: This number is essential for processing the exemption. Omitting it may result in the form being rejected.

Using an outdated version of the form: Always check that you are using the most recent version of the S-3C form. Using an older version can lead to compliance issues.

Incorrectly identifying the type of exemption: Make sure to select the appropriate exemption category that applies to your project. Misclassification can lead to tax liabilities.

Failing to sign and date the form: The signature of the buyer or authorized agent is crucial. Without it, the form is incomplete and invalid.

Not providing a valid project starting and completion date: These dates help establish the timeline for the exemption. Missing dates can raise questions about the project's validity.

Submitting the form to the wrong entity: The S-3C form should be filed with the seller, not with the Vermont Department of Taxes. Misplacing the form can lead to unnecessary complications.

Overlooking the requirement for supporting documentation: When using a multiple purchase exemption certificate, ensure that each invoice links back to the exemption certificate to validate the purchases.

Vermont Sales Tax Exemption Certificate

for

CONTRACTORS COMPLETING A QUALIFIED EXEMPT PROJECT

(listed below)

32 V.S.A. §

FORM

Complete one exemption certificate for EACH project

|

|

To be filed with the SELLER, not with the VT Department of Taxes. |

|

||

|

|

c Single Purchase - Enter Purchase Price $ _________________ |

|||

|

|

c Multiple Purchase (effective for subsequent purchases.) |

|

||

|

|

|

|

|

|

|

Name |

|

Federal ID Number |

|

|

CONTRACTOR |

|

|

|

||

Business Name |

|

For Individuals/Partnerships |

|||

|

|

Social Security |

|

||

|

|

Number |

|

||

Address |

|

Telephone Number |

|

||

|

|

|

|

|

|

|

City |

|

State |

|

ZIP Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

Seller's Name |

|

|

|

|

SELLER |

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

City |

|

State |

|

ZIP Code |

|

|

|

|

|||

|

|

|

|

|

|

ORGANIZATION

Organization's Name

Address

City

Exempt as:

State

ZIP Code

EXEMPT

c501(c)(3) Registered in Vermont. Vermont Sales and Use Tax Account Number_________________________

cUnited States of America - Agency ____________________________________________________________

cState of Vermont or Subdivision - Name ________________________________________________________

cLocal Development Corporation covered by 10 V.S.A., Chapter 12

cQualifying Manufacturing Facility 32 V.S.A. § 9741(39)

Project

Starting Date

Approximate Completion Date

I certify that I have read and complied with the instructions provided with respect to the use of this Exemption Certificate. I further certify that the above statements are true, complete, and correct, and that no material information has been omitted.

Signature of Buyer or Authorized Agent |

Title |

Date |

FORM

This form may be photocopied. |

Rev.11/19 |

Instructions for Use of the Certificate of Exemption for Contractors (Form

(For use only in completion of qualified projects for exempt organizations)

All tangible personal property purchased by a contractor is taxable as the contractor is considered to be the

•When the contractor is working with a qualifying exempt organization

•When the contractor is working on a specific qualifying exempt project

Tangible personal property exempted from tax must be incorporated into the real estate, or the supplies must be used or consumed on the job. If the contractor buys materials or supplies exempt from tax but uses them later in a taxable project, the contractor must pay use tax on those materials and supplies. Purchases of equipment and tools used by the contractor are subject to tax.

Qualifying Organizations & Projects

A qualifying organization contracts to construct, reconstruct, alter, remodel, or repair any building structure or public works project owned by the Federal government, State of Vermont (and its agencies and subdivisions), or a 501(c)(3) as designated by the Internal Revenue Service and registered with the Vermont Department of Taxes. Please note that many nonprofit organizations, such as civic, social, and fraternal organizations, are not 501(c)(3)s and not all 501(c)(3)s projects qualify for exemption. To qualify, the project must be used exclusively for public purposes, and the project contract must be granted by an exempt organization. Turnkey projects are not exempt, even if the ultimate owner may be an exempt organization.

Qualifying Manufacturing Facility

Under 32 V.S.A. § 9741(39), Sales of building materials within any three consecutive years in excess of $1,000,000.00 in purchase value used in the construction, renovation, or expansion of facilities which are used exclusively, except for isolated or occasional uses, for the manufacture of tangible personal property for sale.

Acceptance in “Good Faith”

A seller who accepts an exemption certificate in “good faith” is relieved of liability for collection or payment of

the Vermont Sales and Use Tax otherwise due on tangible personal property covered by the certificate. Good faith depends upon a consideration of all the conditions surrounding the transaction. To receive an exemption in good faith, a seller is presumed to be familiar with the law and the regulations pertinent to the business in which the seller deals. In order for good faith to be established, all of the following conditions must be met:

a.The buyer must present the certificate prior to or at the time of the purchase of the property.

b.The certificate must contain no statement or entry which the seller knows, or has reason to know, is false or misleading.

c.The certificate is on an exemption form issued by the Vermont Department of Taxes or a form with substantially identical language.

d.The certificate must be dated and complete and in accordance with published instructions.

e.The Vermont Sales and Use Tax account number is provided on the certificate where applicable

f.The property to be purchased is of a type ordinarily used by the buyer for the purpose described on the certificate.

Improper Certificate/Lack of Certificate

Sales of tangible personal property subject to tax which are not supported by properly executed exemption certificates are taxable retail sales. The burden of proof that the tax was not required to be collected is upon the SELLER.

Retention of Certificates by the Seller

Sellers must retain exemption certificates for at least three years from the date of the last sale covered by the certificate to document why tax was not collected from the buyer.

Multiple Purchase Exemption Certificates

If the buyer presents a “Multiple Purchase” exemption certificate to the seller, it may be used only when purchasing tangible personal property for use on the qualified exempt project as noted on this exemption certificate. For each purchase covered by the exemption certificate, the sales slip or invoice must show the buyer’s name and address sufficient to link the purchase to the exemption certificate on file.

Other types of exemption certificates that may be applicable are available on our website at: www.tax.vermont.gov. For questions regarding how these exemption certificates may be properly applied, please contact the Vermont Department of Taxes at (802)

FORM

Page 1 of 1 Rev. 11/19

The following is a list of documents that are commonly used alongside the S 3C Vermont form. Each document serves a specific purpose in the context of sales tax exemptions for contractors working on qualified exempt projects.

These documents are essential for ensuring compliance with Vermont's sales tax regulations. Proper use of these forms can help contractors and organizations effectively manage their tax obligations while benefiting from applicable exemptions.

Do You Have to Take Mpje for Each State - The Pharmacist Manager may submit required statements on pharmacy letterhead or using a provided form.

The California ATV Bill of Sale form is crucial for documenting the sale and transfer of an all-terrain vehicle, ensuring that both the buyer and seller have an official record of their transaction. This document not only provides essential details about the sale but also serves as proof necessary for registration and legal purposes. To find more about necessary paperwork, you can check out All California Forms, which offers a variety of templates and resources for California residents.

Vermont Income Tax Forms - Specify your occupation and whether you are 65 years old or older for potential benefits.