Legal Promissory Note Template for Vermont

Legal Promissory Note Template for Vermont

The Vermont Promissory Note form serves as a crucial financial instrument for individuals and businesses seeking to formalize a loan agreement. This document outlines the terms under which one party, the borrower, agrees to repay a specified amount of money to another party, the lender, typically within a predetermined timeframe. Key aspects of the form include the principal amount borrowed, the interest rate applicable to the loan, and the repayment schedule, which details how and when payments will be made. Additionally, the form may specify any collateral offered to secure the loan, thereby providing the lender with assurance in case of default. The inclusion of signatures from both parties is essential, as it indicates mutual consent to the terms outlined in the document. By establishing clear expectations, the Vermont Promissory Note helps to protect the rights of both the lender and the borrower, fostering a transparent and accountable lending relationship.

When filling out the Vermont Promissory Note form, it is important to follow certain guidelines to ensure the document is completed correctly. Below is a list of things to do and avoid during this process.

A loan agreement is a formal contract between a borrower and a lender. Like a promissory note, it outlines the terms of a loan, including the amount borrowed, interest rates, and repayment schedule. However, a loan agreement is generally more comprehensive, often including additional clauses that address collateral, default conditions, and other legal obligations. Both documents serve to protect the interests of the lender while ensuring the borrower understands their responsibilities.

A mortgage is another document that shares similarities with a promissory note. It is used when borrowing money to purchase real estate. The promissory note represents the borrower's promise to repay the loan, while the mortgage secures the loan with the property itself. If the borrower defaults, the lender can take possession of the property through foreclosure. This dual structure provides security for the lender and clarity for the borrower.

A security agreement is similar in that it creates a secured transaction. This document outlines how a borrower can offer collateral to secure a loan. Like a promissory note, it specifies the terms of repayment and the consequences of default. However, a security agreement focuses on the collateral itself, detailing what happens to it if the borrower fails to meet their obligations. Together, these documents provide a clear framework for both parties.

An installment agreement is another related document. This type of agreement lays out a plan for repaying a debt in regular installments over time. Similar to a promissory note, it defines the amount owed, payment frequency, and interest rates. The key difference lies in the structure of repayment; installment agreements typically involve multiple payments, while a promissory note may allow for a lump-sum payment at the end of the term.

A personal guarantee is a document that can accompany a promissory note, especially in business transactions. This guarantee is a promise made by an individual to repay a loan if the primary borrower defaults. While a promissory note binds the borrower, a personal guarantee provides additional security for the lender, ensuring that someone with personal assets is accountable for the debt.

When dealing with transactions such as the sale of an RV, it’s essential to utilize a proper documentation process to ensure clarity and legality. One important document in this context is the Texas RV Bill of Sale form, which not only confirms the sale but helps in the official transfer of ownership and title registration. For more details on this process, you can refer to TopTemplates.info.

A lease agreement shares similarities with a promissory note when it comes to rental payments. Both documents outline the terms of payment, including amounts and due dates. A lease agreement, however, is specifically for renting property and includes terms about the duration of the lease, responsibilities of both parties, and conditions for termination. In essence, both documents create a financial obligation between parties.

A deed of trust is closely related to a promissory note, particularly in real estate transactions. It involves three parties: the borrower, the lender, and a trustee. The borrower signs a promissory note to repay the loan, while the deed of trust secures that loan with the property. If the borrower defaults, the trustee has the authority to sell the property to satisfy the debt, similar to the mortgage process.

A credit agreement is another document that bears resemblance to a promissory note. It outlines the terms under which a borrower can access credit from a lender. This agreement typically includes details about interest rates, repayment terms, and fees. While a promissory note is a promise to repay a specific loan, a credit agreement can provide access to a revolving line of credit, offering more flexibility for the borrower.

An acknowledgment of debt is a simpler document that serves to confirm that a debt exists. Like a promissory note, it outlines the amount owed and may include terms of repayment. However, it often lacks the detailed provisions found in a promissory note. This document can serve as a useful tool for both parties, providing a written record of the debt without the complexity of a full loan agreement.

Finally, a forbearance agreement may also resemble a promissory note in its purpose of addressing a debt. This document is used when a lender agrees to temporarily postpone or reduce payments due to the borrower's financial hardship. It outlines the new terms and conditions for repayment, ensuring both parties are clear about their obligations during the forbearance period. While it modifies the original loan terms, it still maintains the fundamental promise to repay the debt.

Incorrect Names: People often misspell their names or the names of the parties involved. Always double-check the spelling to ensure accuracy.

Missing Dates: Failing to include the date of the agreement can lead to confusion. Always specify the date when the note is signed.

Improper Loan Amount: Some individuals write the loan amount incorrectly. Make sure to write both the numerical and written forms of the amount for clarity.

Omitting Payment Terms: Clearly outline the repayment schedule. Not specifying how and when payments will be made can create misunderstandings.

Ignoring Interest Rates: Some people forget to include the interest rate or miscalculate it. Always state the interest rate explicitly if applicable.

Not Initialing Changes: If any changes are made to the form, failing to initial those changes can lead to disputes. Always initial any alterations.

Signing in the Wrong Place: Ensure that signatures are placed in the correct section of the document. Misplaced signatures can invalidate the note.

Not Including Witnesses or Notary: Depending on the situation, some promissory notes may require witnesses or notarization. Check if this is necessary.

Neglecting to Keep Copies: After completing the form, failing to make copies for all parties involved can lead to issues later. Always keep a copy for your records.

Using Incomplete Information: Providing incomplete information about the borrower or lender can cause problems. Ensure all fields are filled out completely.

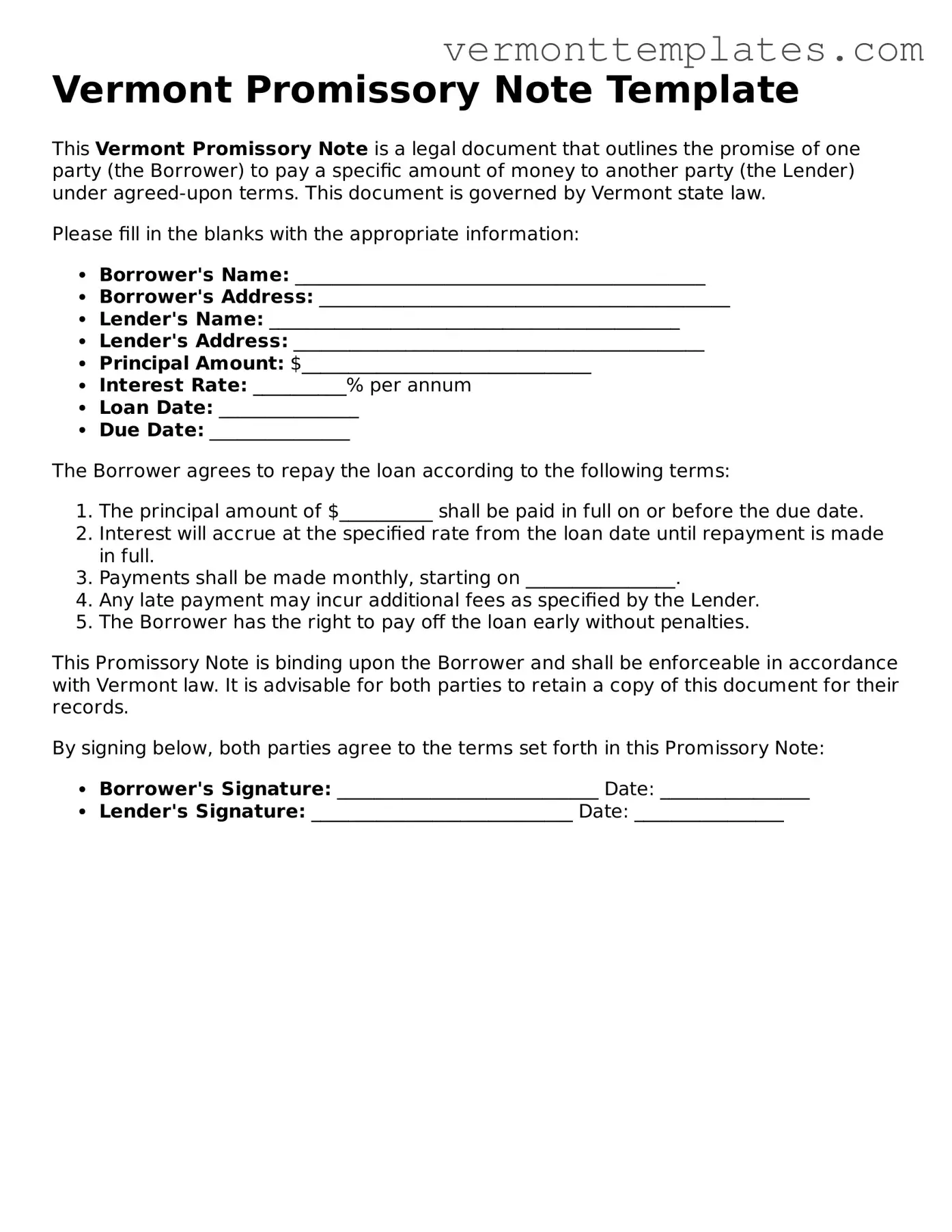

Vermont Promissory Note Template

This Vermont Promissory Note is a legal document that outlines the promise of one party (the Borrower) to pay a specific amount of money to another party (the Lender) under agreed-upon terms. This document is governed by Vermont state law.

Please fill in the blanks with the appropriate information:

The Borrower agrees to repay the loan according to the following terms:

This Promissory Note is binding upon the Borrower and shall be enforceable in accordance with Vermont law. It is advisable for both parties to retain a copy of this document for their records.

By signing below, both parties agree to the terms set forth in this Promissory Note:

In the context of lending and borrowing, various forms and documents often accompany the Vermont Promissory Note. Each of these documents serves a specific purpose, ensuring clarity and legal compliance in financial transactions. Below is a list of commonly used documents that may be associated with a Vermont Promissory Note.

Each of these documents plays a crucial role in the lending process, helping to establish clear expectations and protect the interests of both lenders and borrowers. Understanding these forms can facilitate smoother transactions and reduce the potential for disputes.

Vermont Bill of Sale for a Vessel - This form provides a legal record of the sale, protecting both buyer and seller.

The California ATV Bill of Sale form is not only essential for documenting the transfer of an all-terrain vehicle, but it also aligns with other necessary paperwork that sellers and buyers should be aware of, including All California Forms to ensure a smooth transaction process.

Are Employers Required to Provide Employee Handbook - The company’s code of ethics is outlined within these pages.

Does Delaware Require an Operating Agreement for Llc - The agreement can detail individual member duties and contributions to the LLC.